Insurance Coverage for Weight Loss Shots: What Americans Need to Know

Daniel Zvi

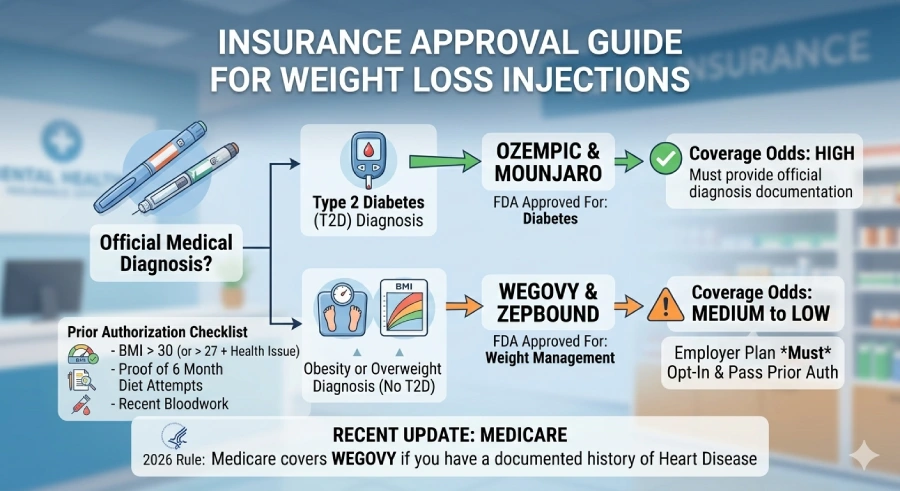

If you are trying to figure out if your US health insurance will cover weight loss injections, the short answer is: it depends entirely on your specific policy and your health history. Generally, getting your insurance company to say "yes" comes down to three main factors: 1) The specific drug's official label (whether it is approved for diabetes or strictly for weight loss), 2) Your employer's specific insurance package (whether they opted-in to cover obesity treatments), and 3) Passing a "Prior Authorization" (a process where your doctor proves to the insurance company that you actually need the medicine).

![]() Our top picks for April 2026

Our top picks for April 2026

The Golden Rule: Diabetes vs. Weight Loss

The biggest point of confusion at the pharmacy counter comes down to what the FDA officially approved the medication to do. Insurance companies treat diabetes and weight loss very differently.

Shots for Type 2 Diabetes (Ozempic & Mounjaro)

If you have an official Type 2 diabetes diagnosis, getting insurance to cover these shots is usually a pretty smooth process. Because Ozempic and Mounjaro are officially categorized as diabetes care, health insurance plans almost always cover them as necessary medical treatments to keep your blood sugar in check.

Shots for Weight Loss (Wegovy & Zepbound)

Here is where it gets tricky. Wegovy and Zepbound contain the exact same active ingredients as their diabetes counterparts, but they are officially labeled for weight loss. Historically, insurance companies have treated weight loss as a "lifestyle" choice rather than a medical necessity, making these specific brands much harder to get covered without jumping through major hoops.

The Quick Guide to Insurance Approval Odds

| Brand Name | What’s Inside It? | What the FDA Approved it For | Insurance Approval Odds |

| Ozempic | Semaglutide | Type 2 Diabetes | High: Usually covered if you have an official diabetes diagnosis. |

| Mounjaro | Tirzepatide | Type 2 Diabetes | High: Usually covered if you have an official diabetes diagnosis. |

| Wegovy | Semaglutide | Weight Loss & Heart Health | Medium to Low: Needs a special employer plan, unless you have a history of heart disease. |

| Zepbound | Tirzepatide | Weight Loss | Low: Almost always requires your employer to specifically buy "weight loss coverage." |

The "Heart Health" Loophole: A New Way to Get Covered

Over the last year, a massive shift happened in how insurance companies view these medications, largely thanks to new clinical data.

Does having heart disease change my coverage?

Yes, dramatically. The FDA recently approved Wegovy specifically to reduce the risk of major cardiovascular events (like heart attacks and strokes) in adults who are overweight and have a history of heart disease. Because of this new label, many insurance plans that normally refuse to cover weight loss drugs will now approve Wegovy if your doctor proves you have existing cardiovascular disease. ## Who Actually Pays for It? (Breaking Down Plan Types)

Having a big-name insurance company on your ID card doesn't automatically mean you have coverage. It actually comes down to who is buying the plan.

Employer-Sponsored Insurance

Here is the biggest secret in health insurance: your employer decides what is covered, not just the insurance company. When your company buys a health plan for its employees, they have to pay extra to add "weight loss coverage" to the package.

Why are some employers dropping coverage?

Because these medications are incredibly expensive and wildly popular, they are costing companies millions of dollars a year. Recently, many employers have started dropping their weight loss coverage entirely or putting massive restrictions on it simply because the company cannot afford the premium hikes. If your boss decided to save money and skip the add-on, the insurance company will automatically deny your prescription.

Medicare & Medicaid Updates

For a long time, federal law banned Medicare from covering drugs used purely for weight loss. However, the landscape has shifted:

- The Heart Disease Exception: Medicare Part D plans are now allowed to cover Wegovy, but only if you have a documented history of heart disease. They still will not cover it if you only have a high BMI.

- New Pricing Models: Thanks to recent federal negotiations, some eligible Medicare and Medicaid patients are finally seeing direct-to-consumer price caps to help ease the burden.

- Medicaid: Coverage still varies wildly depending on which state you live in, with some states mandating coverage and others completely excluding it.

The "Prior Authorization" Battle Explained

Even if your plan covers weight loss medication, they won't just hand it over. They will almost always ask for a "PA."

What is a Prior Authorization (PA)?

Think of a Prior Authorization as an extra permission slip. It is a formal process where your doctor has to send paperwork to the insurance company proving that you meet all their strict rules before the insurance company will agree to pay the pharmacy.

What do they look for?

Every insurance plan is different, but they usually want to see a few specific things to approve your permission slip:

- A specific Body Mass Index (usually a BMI over 30, or over 27 if you also have something like high blood pressure or sleep apnea).

- Proof that you have actively tried and failed traditional diet and exercise programs for at least six months.

- Recent blood work to show your overall health baseline.

Generics vs. Compounded Shots: The Cost Workarounds

If your traditional insurance flat-out refuses to pay for brand-name Wegovy or Zepbound, you do not necessarily have to pay the $1,000+ retail price. However, you need to know the massive difference between the two cheaper alternatives on the market right now.

1. The New FDA-Approved Generic (Liraglutide)

In late 2025/early 2026, the FDA approved the very first true generic weight loss shot (a generic version of an older drug called Saxenda).

- Does insurance cover it? Because it is an official, FDA-approved generic, insurance companies are much more likely to cover this than the expensive brand names.

- The catch: Unlike Wegovy or Zepbound, which are taken once a week, this generic option is a daily injection, and it generally results in slightly less overall weight loss than the newer weekly shots.

2. The Telehealth Alternative (Compounded Shots)

Because navigating traditional insurance can take months, many people turn to online telehealth clinics. These platforms prescribe "compounded" versions of the medication, which are custom-mixed by a specialized pharmacy rather than made in a massive factory.

- Does insurance cover compounded shots? No. Almost never. Insurance companies will not pay for compounded weight loss medicine because it is not officially FDA-approved.

- The catch: If you go this route, you will be paying strictly out-of-pocket (cash pay). However, the flat monthly fee for a compounded shot is usually a fraction of the cost of the brand-name retail price.

Here are the Top-Rated telehealth services for fast access to weight loss injections:

![]() Our top picks for April 2026

Our top picks for April 2026

3. Manufacturer Savings Programs

If you want to stick with the brand names but your commercial insurance denied you, the companies that make these drugs offer direct-to-consumer savings cards on websites like NovoCare and LillyDirect. If you qualify, these official programs can often bring the cash price down to anywhere between $149 and $449 a month.

4. Use Your HSA or FSA Funds

If you have a Health Savings Account (HSA) or a Flexible Spending Account (FSA) through your employer, you can absolutely use that pre-tax money to pay for your weight loss shots. Whether you are paying a $50 copay at the pharmacy, paying cash for a compounded shot online, or using a manufacturer's discount, using your HSA card softens the financial blow by letting you use tax-free dollars.

Frequently Asked Questions

Q: Will my insurance cover a weight loss shot just because I am overweight?

A: Usually, no. Being overweight is rarely enough on its own. Insurance companies almost always require a high BMI plus another documented health condition (like sleep apnea or heart disease), or your specific policy must have a special "weight management" clause built into it.

Q: Why does my friend's insurance cover it, but mine doesn't?

A: Because insurance rules depend entirely on the specific plan your employer chose to buy. You and your friend could both have the exact same insurance provider, but if their company paid for the weight loss add-on and your company didn't, their shot will be covered and yours won't.

Q: Can I just pay cash at the pharmacy if my insurance denies me?

A: Yes, you can always choose to pay out-of-pocket without insurance. However, the standard retail cost at a local pharmacy is typically between $1,000 and $1,350 per month. If you are paying cash, you are much better off using the manufacturer's direct-to-consumer discount programs or exploring the generic option.

Q: What is a "step therapy" requirement?

A: Step therapy is when your insurance company forces you to try a cheaper, older weight loss pill or a generic injection first. If that cheaper option doesn't work for you after a few months, only then will the insurance company agree to pay for the newer, more expensive brand-name shots.

Liked this article?

Smart Recommendations

Thank you!